Conference of Principal Code Compliance Officers (PCCOs) / Chairmen of Regional Rural Banks organised by BCSBI at Mumbai, on July 15, 2013 (Inaugural Address by Dr. (Smt.) Deepali Pant Joshi, Executive Director, Reserve Bank of India)

It is a privilege to be here this morning and I would like to thank Shri A.C. Mahajan, Chairman, BCSBI, and Shri N. Raja, CEO, BCSBI, for giving me the opportunity to be here. I extend warm congratulations to the BCSBI on the initiative of hosting this Conference of Principal Code Compliance Officers (PCCOs) of Regional Rural Banks (RRBs). I understand it is an annual event.

2. The purpose is to interface with the Chairmen of RRBs. This becomes especially important as we all accept that the quality of customer service and the bank™s treatment of customers depend on guidance of its Top Management in the building of an organization culture committed to high level of customer service with an ethical value system.

3. The Banking Codes and Standards Board of India (BCSBI) was set up seven years ago, since then it has prepared and published voluntary comprehensive Codes and Standards for banks for providing fair treatment to customers.

4. It functions as an independent body to monitor and to ensure that the Codes voluntarily adopted by banks are adhered to, in true spirit in delivering the services, as promised.

BCSBI had evolved two Codes for Member Banks to implement:

- Code of Bank™s Commitment to Customers

- Code of Bank™s Commitment to Micro and Small Enterprises

These Codes are periodically updated keeping in view the contemporary recent changes.

5. Now let us talk a bit about RRBs:

The RRBs are now treated on par with other commercial banks and as banks, they must focus on customer empowerment and extending customer service. I have been a Director of several RRBs many years ago and have keenly watched their evolution. I will now spend some time in discussing their evolution and growth.

Establishment of RRBs

6. The Narasimham Working Group (1975) conceptualized the creation of RRBs in 1975 as a new set of regionally oriented rural banks, which would combine the local feel and familiarity of rural problems characteristic of cooperatives with the professionalism and large resource base of commercial banks. Regional Rural Banks (RRBs) were established under the Regional Rural Banks Act, 1976 to create an alternative channel to the cooperative credit structure and to ensure sufficient institutional credit for the rural and agriculture sector. RRBs are jointly owned by the Government of India, the concerned State government and sponsor banks, with the issued capital shared in the proportion of 50 percent, 15 percent and 35 percent, respectively. As per the provisions of the Regional Rural Banks Act, 1976 the authorized capital of each RRB is Rs. 5 crore and the issued capital is a maximum of Rs. 1 crore.

7. From a modest beginning of 6 RRBs with 17 branches covering 12 districts in December, 1975 the number of RRBs increased to 196 RRBs with 14,446 branches in 1991 operating in 518 districts across the country. After a phase of consolidation starting from September, 2005, the number of RRBs was reduced from 196 to 82. In the current phase of consolidation which began in October, 2012 by amalgamation of RRBs across sponsor banks within a State, the number of RRBs has further reduced to 61 RRBs as on date with over 18000 branches in 638 districts.

Reforms in the RRB Sector have taken place in three phases :

First Phase: 1993-2000

8. Based on the recommendations of the Narasimham Committee Report (1992), reforms were initiated in 1993 with a view to improve the financial health and operational viability of RRBs. Various measures including recapitalization, rationalization of branch network, providing better access to non fund business, expanding avenues of investment and advances, upgrading the level of technology and taking up select RRBs for comprehensive restructuring were taken. Further, they were permitted to lend to non-target group borrowers up to 60 per cent of new loans. From January, 1995 the investment avenues for RRBs were broadened to improve the operational efficiency and profitability. In December, 1996 the investment policy was further liberalised, to accord parity with commercial banks, permitting RRBs to invest in shares and debentures of corporate and units of Mutual Funds with a ceiling upto 5% of the incremental deposits of the bank during the previous year. Prudential accounting norms of income recognition, asset classification, provisioning and exposure, were implemented during this period to provide durability to the reform process. In April, 2000, RRBs were allowed to apply for permission to maintain non-resident accounts in rupees.

Second Phase: 2004-2010

9. The next Phase of reforms started in 2004-05 with the structural consolidation of RRBs by amalgamation of RRBs of the same sponsor bank within a State. Capital support aggregating Rs. 1796 crore was provided during the period 2007-08 to 2009-10 as part of this process. In October, 2004, RRBs were permitted to undertake insurance business without risk participation and in May, 2007 they were allowed to take up corporate agency business for distribution of all types of insurance products without risk participation. In December, 2005, to further extend support to RRBs for accelerating the flow of credit to the rural areas, the resource base of RRBs was expanded to include lines of credit from sponsor banks; they were also permitted to access the term money markets and CBLO/Repo markets. Issuance of credit/debit cards, setting up of ATMs, opening of currency chests, undertaking government business, as subagents, were allowed to enhance business opportunities. In March, 2006, RRBs were permitted to apply for AD-Category II licence to undertake non-trade related current account transactions for certain specified purposes to further enhance the scope of business. In June, 2007 to increase their exposure to foreign exchange business they were allowed to accept FCNR deposits. RRBs were also allowed to participate in consortium lending with sponsor banks, DFIs and other banks within the area of operation. The capital adequacy standards were introduced in December, 2007 in the context of financial stability and RRBs were required to disclose the level of CRAR in their balance sheets.

Third Phase: 2010 onwards

10. Based on the recommendations of Dr. K. Chakrabarty Committee (2010), 40 RRBs have been taken up for recapitalization to enable them to achieve and sustain a CRAR of 9%. In November, 2010 the branch licensing policy was liberalized which allowed RRBs to open branches in Tier 3 to Tier 6 centres (with population of up to 49,999 as per 2001 Census) without prior approval from the Reserve Bank, subject to certain conditions. This policy was further liberalized in August, 2013 to also include Tier 2 centres. The second phase of consolidation commenced from October, 2012 with amalgamation of RRBs across sponsor banks within a State.

Performance of RRBs Post Amalgamation:

11. It can be seen from the data on performance of RRBs post amalgamation that there has been consistent progress in the operations of RRBs.

|

2005-06 |

2006-07 |

2007-08 |

2008-09 |

2009-10 |

2010-11 |

2011-12 |

2012-13(P) |

|

| No of RRBs |

133 |

96 |

90 |

86 |

82 |

82 |

82 |

64 |

| No of branches |

14489 |

14563 |

14790 |

15524 |

15475 |

16024 |

16914 |

17867 |

| Net profit (cr) |

617 |

625 |

1027 |

1335 |

1884 |

1785 |

1886 |

2384 |

| Profit/loss making RRBs |

111/22 |

81/15 |

82/8 |

80/6 |

79/3 |

75/7 |

79/3 |

63/1 |

| Deposits (cr) |

71329 |

83144 |

99093 |

120189 |

145035 |

166232 |

186336 |

211457 |

| Loans & Advances (cr) |

38520 |

47326 |

57568 |

65609 |

79157 |

94715 |

113035 |

133098 |

| CD ratio (%) |

55.7 |

58.3 |

59.5 |

56.4 |

57.6 |

59.51 |

63.3 |

66.13 |

| Share of CASA in deposits (%) |

59.14 |

61.21 |

59.63 |

58.35 |

57.90 |

60.35 |

58.51 |

57 |

| Share of PSA in total |

81 |

82.2 |

82.9 |

83.4 |

82.2 |

83.5 |

80 |

86 |

| Share of agri adv to total (%) |

54.2 |

56.6 |

56.3 |

55.1 |

54.8 |

55.7 |

53 |

63 |

| Gross NPA (%) |

7.3 |

6.55 |

6.1 |

4.2 |

3.72 |

3.75 |

5.03 |

5.65 |

| Net NPA % |

|

3.46 |

3.36 |

1.81 |

1.62 |

2.05 |

2.98 |

3.40 |

| Source: Reports on Trend and Progress of Banking in India and NABARD | ||||||||

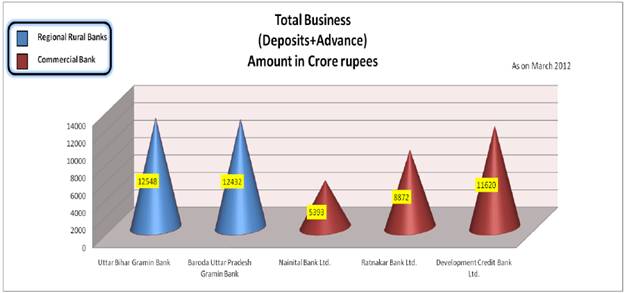

Post amalgamation, in terms of total business 2 RRBs are larger than some private sector commercial banks as can be seen from the graph below

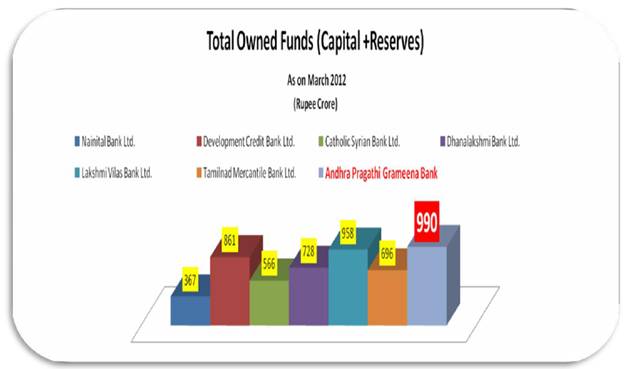

In terms of owned funds Andhra Pragathi Grameena Bank is much larger than some of the private sector commercial banks.

Financial Inclusion by RRBs

12. In order to achieve the objective of universal financial inclusion, RRBs have been directed to use a combination of strategies, which include (a) provision of basic banking products; (b) introduction of the Business Correspondent/Business Facilitator (BF) model; (c) adoption of the relaxed regulatory Know Your Customer (KYC) guidelines; (d) enhanced use of technology; and (e) setting up financial literacy centres in districts to achieve greater outreach. Though the share of RRBs in aggregate deposits and gross bank credit is only around 2.5 to 3 per cent, they play a critical role in financial inclusion. RRBs are required to prepare Financial Inclusion Plans which are to be integrated with their business plans. The major highlights of their performance under the first FIP for the period April, 2010-March, 2013 are as under.

1. Banking Outreach

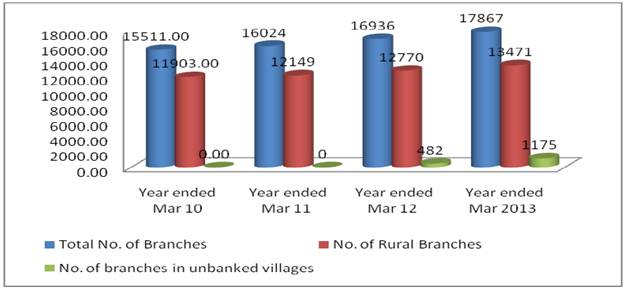

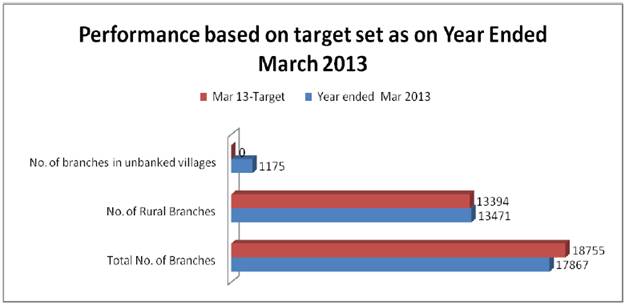

The number of rural branches has increased by 15%. The self set FIP targets have almost been met. At the same time number of branches in unbanked villages has grown from 0 in 2011 to 1175 as on year ended March, 2013. However, they could not completely full fill their targets of opening up the total number of branches. The target was set around 18,755 branches while they were able to open close to 17,867 branches only as on year ended March 2013.

2. Type of Banking Outlets- Based on Size of Population

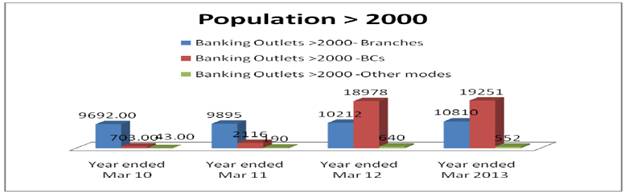

a. Population > 2000

The total number of banking outlets can be viewed in terms of Bank Branches, Business Correspondents (BCs) and Other Modes. For villages with population of more than 2,000 there has been a considerable increase in the number of BCs. There was a steep rise from mere 703 BC outlets (year ended March, 2010) to close to 19,000 BC outlets (year ended March, 2012).

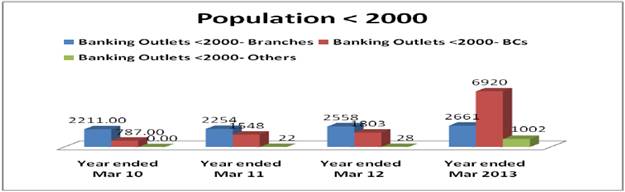

b. Population < 2000

For villages with population less than 2000, the number of BCs registered a sharp growth. However, the RRBs failed in achieving the set target for BC outlets for the year ended March, 2013.

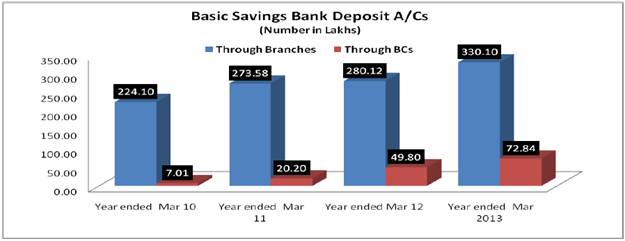

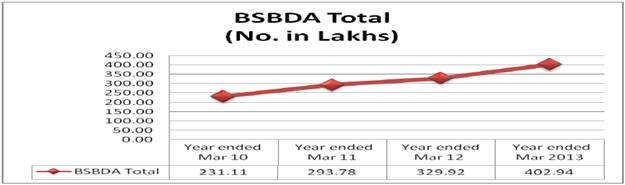

3. Basic Savings Bank Deposit Account

It is observed that most of the Basic Savings Bank Deposit Accounts (BSBDA) were opened through branches. The number of accounts opened through branches stood at 330.10 lakh, while only 72.84 lakh accounts were opened through BCs (year ended March 2013)

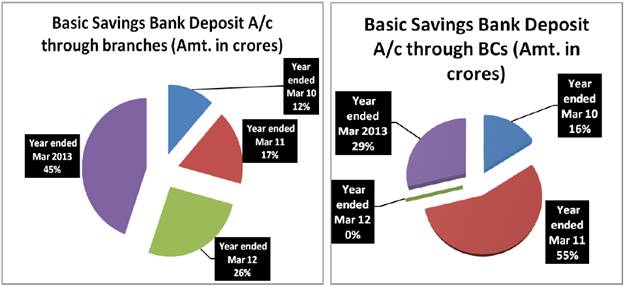

The graphs show the amount mobilized each year (in percentage) in Basic Savings Bank Deposit Account (BSBDA) through branches and BCs. In the year 2012, there was a sharp fall in the amount mobilized through BCs but it has again picked up in 2013.

The total number of Basic Savings Bank Deposit Accounts has increased considerably. From around 230 lakh accounts (year ended March, 2010) to more than 400 lakh accounts (year ended March, 2013), the growth rate has been equal to 74%.

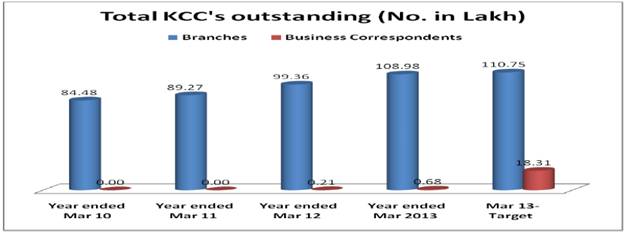

4. Kisan Credit Cards

The branches were successful in achieving their target number of KCCs (year ended March, 2013). No KCCs were sourced through the BCs for the years ended 2010 and 2011.

5. General Credit Cards

13. The BC is utilized to externalize part of the credit cycle. He has to work towards spreading awareness of the availability of the bank™s products and services. BCs can be better leveraged by the RRB branches. They are in need of greater handholding and necessarily of close and continuous supervision.

14. Though there has been reasonable progress with regard to extending the penetration of banking services and opening of basic bank accounts, the number of transactions through the ICT based BC outlets are poor. During the period of the next 3 year Financial Inclusion Plan i.e. 2013-16 RRBs should endeavour to leverage technology to the optimum. Technology enables the bank to transcend the barriers of geography and to provide services at the borrower™s doorstep. Though the initial cost is high over time it pays for itself. Regional Rural Banks should through financial innovation try to focus on mezzanine finance, on the creation of customised products linked to the income streams of the poor borrowers and geared to meet the specific needs of the rural clientele. Mobile technology can be harnessed to improve access and usage of banking services.

The Codes and RRBs

15. All banks offer the same products with variants but what distinguishes and sets apart and gives the competitive edge to a bank is the quality of customer service extended by the bank.

16. The Codes are the RRBs mandate, adopted by RRBs with the specific approval of the Board of Directors. RRBs must take full ownership of these Codes and facilitate their adoption ensuring complete adherence.

17. RRBs have undergone a sea change. They are now almost treated on par with other commercial banks. The customers of the RRBS are illiterate and poor; there is also an asymmetry of information. Hence the adoption of standards of behaviour and codes of conduct framed by BCSBI for dealing with customers is an imperative.

18. At one point we are all customers of banks. What are the ingredients of treating customers fairly? Transparency, proper disclosure, non-discriminatory and non-exploitative pricing, building a robust and responsive grievance redressal mechanism within the bank and also making the customer aware of redressal available through the Banking Ombudsman Scheme. Transparency does not mean bombarding the illiterate customer with humungous amount of information which she is neither able to understand or use. It merely means no hidden charges. The customer must up front understand what she is letting herself in for; the terms and conditions of the contract should be clearly understood.

19. The codes need to be clearly understood and fairly implemented by Regional Rural Banks. Banks are commercial establishments. They are not philanthropic organizations. However, they enjoy great leverage and an oligopolistic position simply as the borrower in the rural areas may lack choice which his urban counterpart enjoys. This casts a much greater responsibility upon the RRBs. Knowledge and general awareness about the Codes of the BCSBI needs to be increased. Just this morning, Mr Mahajan shared with me that despite valiant attempts knowledge of and appreciation of the BCSBI codes was spreading very slowly and this was a cause of concern. The Chairmen of the RRBs must appreciate that the poor borrower who comes to the door step of the Bank is highly unlikely to meet the Chairman of the bank. For him the frontline manager is the Bank. The frontline manager needs to be sensitized to the importance of the Code of Bank™s Commitment to Customers. He must understand and believe in them. This affirmation will then translate to increased sensitivity and in empathetic behavior towards the special niche clientele of the RRBs. The pay off in terms not just of profitability but in terms of job satisfaction assuredly, will be tremendous.

20. To close with a few clear messages for easy recall:

- Please ensure that all the RRB staff are aware of, clearly understand and commit to the BCSBI Codes.

- The Codes are evident in precept and practice and in the actual business of the Banks

- Customer empowerment occurs as knowledge and awareness of customer rights is enhanced .

Once again I thank the BCSBI for this opportunity and commend them on the initiative of hosting this conference.